Breaking the Cycle

Overcoming Financial Procrastination for Legal Professionals

January/February 2025

Download This Article (.pdf)

No one will disagree that those who work in law are under intense pressure. From the very beginning, from their initial college courses to taking the dreaded bar exam, the journey is grueling. Once they start practicing, they face the additional stress of working to make partner and meeting billable-hour mandates. This billing practice demands meticulous time-tracking and often leads to long hours, contributing to high levels of stress and burnout. The relentless focus on accumulating billable hours can often overshadow other important aspects of professional and personal life.

The World Health Organization and the International Labour Organization suggest that each year, three-quarters of a million people die from ischemic heart disease and stroke due to working long hours.1 For legal professionals, the constant demands and extended work hours can exacerbate these risks, leading to serious health issues. Amidst all this pressure and overwork, time becomes a scarce commodity, and financial procrastination starts to become the norm. While stress often gets the blame, procrastination could be the true culprit undermining the mental and physical health of legal professionals. Commonly dismissed as a minor inconvenience, procrastination can have profound and far-reaching consequences, especially for those striving to gain control of their finances. Delayed financial planning can severely impact savings, investments, and overall financial health. By understanding and addressing the root causes and effects of procrastination, legal professionals can uncover the path to a secure and prosperous future for both themselves and their offices.

The Root Cause of Financial Procrastination

For legal professionals, financial procrastination typically arises from a lack of time coupled with the overwhelming task of getting financially organized. The demands of their profession can make the thought of gathering financial data and meeting with a professional seem daunting. Additionally, legal professionals are constantly battling the billable hour; any time not spent on billable work, even during personal activities, feels like lost time. This pressure, combined with the cost of professional fees, often pushes financial planning to the back burner.

Fortunately, advancements in financial technology platforms have made organizing finances more streamlined and efficient, reducing both the time commitment and associated costs needed to establish a comprehensive financial plan. By investing just 15 to 20 minutes to get organized, legal professionals can begin setting up systems that ensure their future earnings aren’t solely reliant on billable hours. This shift in perspective allows them to maximize their hard-earned money. The earlier these financial systems are established, the easier it becomes to create passive income in the future. Investing a small amount of time now will lead to substantial payoffs down the road.

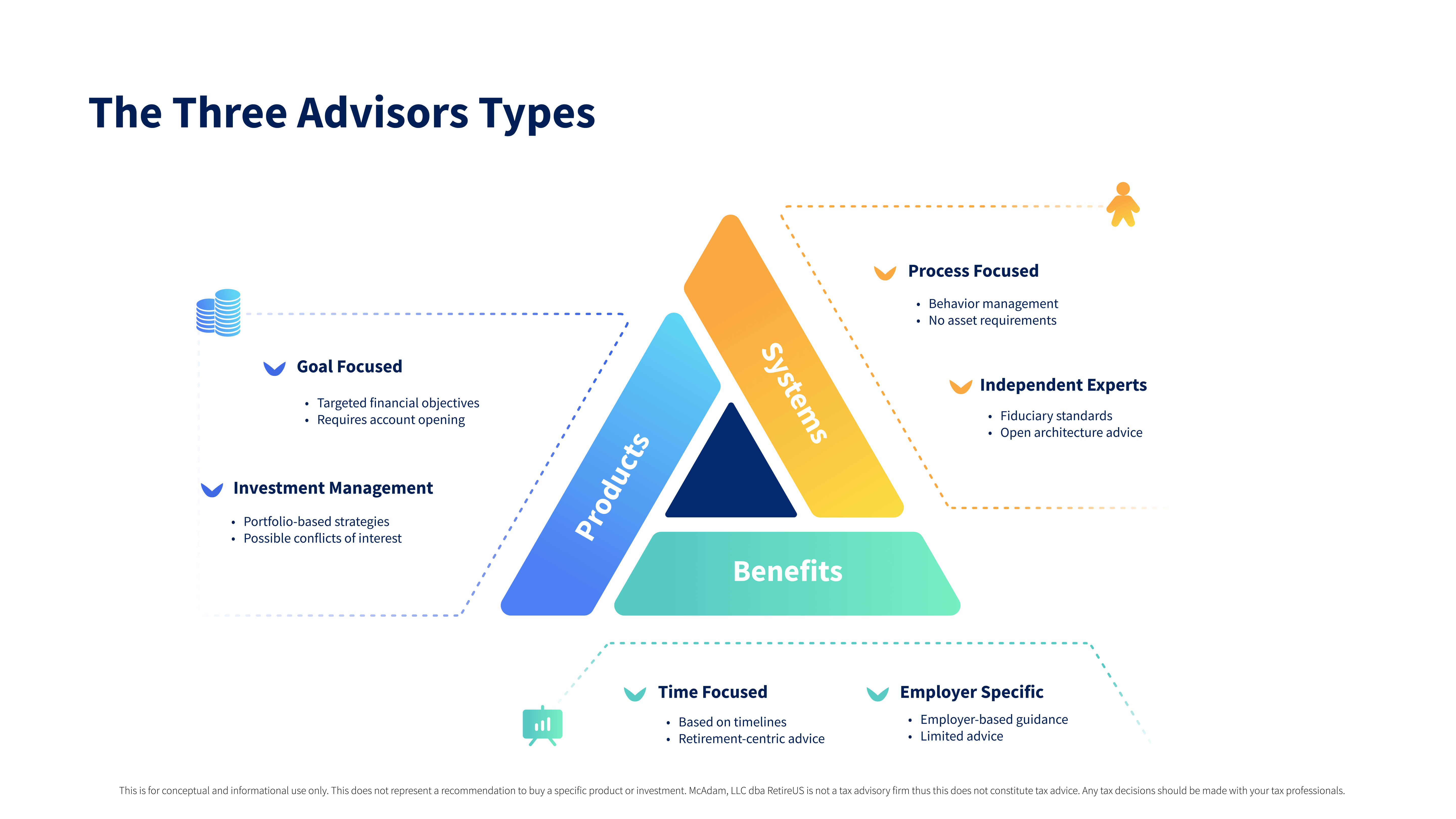

Understanding the Differences in Financial Professionals

When it comes to financial planning, it’s crucial to understand the different types of financial professionals available:

- Workplace benefit professionals: These are the representatives associated with employer-sponsored benefit programs. Their role is primarily to help you navigate your workplace benefits, such as retirement accounts and insurance options. They can assist with understanding fees, fund choices, and the mechanics of your accounts, but they typically do not offer comprehensive financial planning services.

- Product-based advisors: This group dominates the financial advisory industry and is generally nonfiduciary. These advisors are often compensated through commissions or by billing a percentage of the assets they manage. Because of this, their financial advice typically revolves around selling products, such as mutual funds, annuities, or insurance policies. Around 90% of financial advisors in the United States are nonfiduciary.2 This means they are not legally required to prioritize your interests above their own or their institutions.

- Systems-based advisors: The rarest and, until recently, the most cost-prohibitive group, these independent fiduciary financial professionals—often certified financial planners (CFPs)—build personalized financial systems for their clients. Unlike product-based advisors, systems-based advisors take a holistic approach, incorporating various products into a cohesive strategy that supports your financial goals. They also integrate your workplace benefits into this strategy. Due to their unique and independent scope of work, it typically costs around $5,500 per year[3] to work with such professionals and can be challenging to find professionals from this side of the spectrum. In recent years, however, fintech companies have made strides to make these independent professionals more accessible and cost effective.

The True Cost of Waiting

Delaying financial planning can lead to missing out on potentially hundreds of thousands of dollars in savings and investments. There is a pervasive misconception that financial planning is time-consuming and not worth the effort, which deters many professionals from seeking the guidance they need. This delay, however, can be extremely costly.

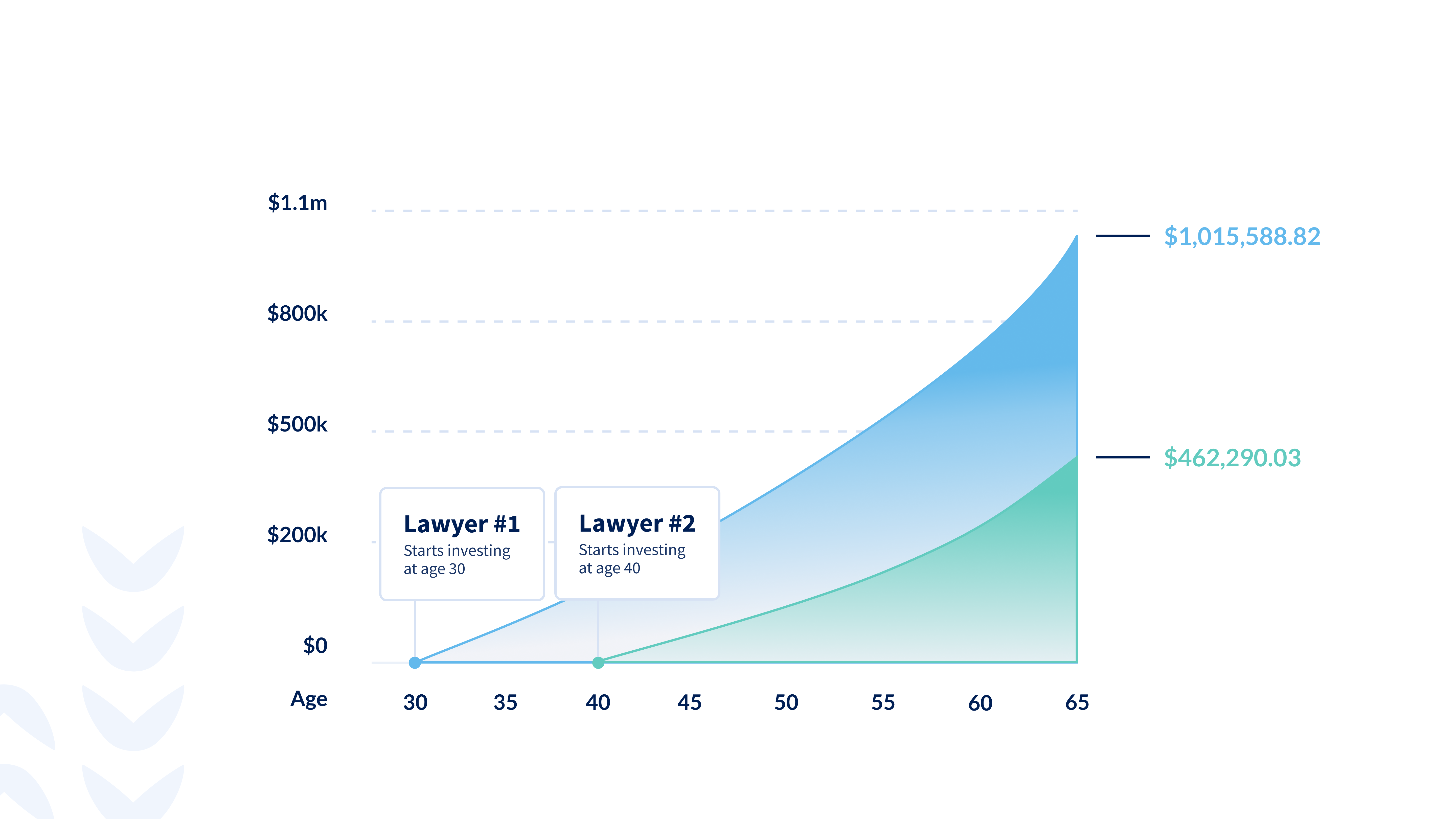

The Impact of Compound Interest

The power of compound interest means that the earlier one starts saving and investing, the greater the potential returns. Compound interest works by earning interest on both the initial principal and the accumulated interest from previous periods. The longer the money is invested, the more it grows exponentially.

For instance, an initial investment of $10,000 with additional savings of $500 a month, starting at age 30 with an average annual return of 7%, would grow to approximately $1,015,589 by age 65. But if the same lawyer waits until age 40 to start investing, the total amount saved would be around $462,290. This decade of procrastination results in a loss of nearly $553,299 in potential retirement funds. This could translate to an additional $25,000 to $35,000 per year in passive income throughout retirement, depending on the withdrawal strategy.

Practical Steps for Immediate Action

Law professionals can take actionable steps now to secure their financial future, which in turn can positively impact their performance and client engagement. Below are some practical steps.

Schedule Regular Financial Reviews

Just as lawyers schedule client meetings and case preparations, dedicating regular intervals to review and manage personal finances is essential. At a minimum, there should be some sort of review at least annually. This can be achieved by blocking time on the calendar specifically for financial planning and delegating tasks to other individuals in the firm to ensure that essential financial tasks are not neglected.

In these financial reviews, focus on five key areas:

- Clarifying your vision: Have a clear, long-term financial vision that aligns with your life goals.

- Setting your targets: Break down your vision into quantifiable short-term and long-term goals.

- Taking inventory of your pacing: Use future value calculations to determine whether you’re on track to meet your financial goals.

- Implementing calculated risk: Based on the return you need to stay on pace and hit your goals, adjust your risk accordingly.

- Prioritizing cash flow: Depending on how well funded your goals are at this point, adjust systematic savings accordingly.

By setting aside dedicated time for financial reviews, lawyers can focus on this critical aspect of their personal and professional lives without feeling overwhelmed.

Seek Authentic Professional Guidance

A downside of seeking advice from an advisor without a fiduciary standard is that they are not legally required to prioritize your best interests above their own or those of their institution. To ensure you’re working with someone who will truly have your best interests at heart, ask potential advisors if they adhere to a fiduciary standard and how they are compensated.

Beyond the common narratives, an advisor can provide insights into areas that benefit both the legal professional and, by extension, their clients. For instance, advisors can offer asset-protection strategies tailored to those in high-liability professions. They can explain how to leverage business structures for tax efficiency, which can have significant long-term benefits. And they can propose philanthropic strategies that not only benefit the community but also enhance the professional’s reputation and their client relationships.

Leverage Technology to Get Organized and Connect With Professionals

Embracing modern technology can significantly transform the way legal professionals approach financial planning. Today’s advanced tools streamline financial management, allowing individuals to efficiently organize their finances and stay aligned with their long-term goals. By using technology to automate and simplify processes like data gathering and financial analysis, professionals can reduce the time and effort typically required for comprehensive financial planning. This not only frees up valuable time but also accelerates the path to meaningful discussions with financial advisors. As a result, legal professionals can optimize their financial strategies without the burden of extensive manual input or the significant cost often associated with traditional planning methods. Integrating technology into financial management empowers legal professionals to make faster, more informed decisions, ultimately enhancing their financial well-being.

The Path to Financial Freedom

Procrastination in financial planning poses significant risks that extend beyond monetary losses. For law professionals, the stakes are particularly high, given the demanding nature of their work. By understanding the true cost of waiting, comparing the time and cost of financial services versus potential financial losses, and taking practical steps for immediate action, legal professionals can secure their financial future. Investing time and resources now into financial planning ensures a prosperous work life that seamlessly transitions into not only a less stressful work life but a fulfilling retirement. The importance of timely financial planning cannot be overstated—it is an investment in one’s future that pays dividends in both financial security and professional well-being.

As we look to the future, the question is not whether legal professionals should prioritize their financial health, but how they can best achieve this. The answer lies in taking action to create proactive and informed financial systems for themselves. This proactive approach will significantly improve their overall quality of life, both now and in the years to come.

Explore This Issue

Management Liability Coverages

Tort and Insurance Law

By Britton D. Weimer

The Past, Present, and Future of Residential Construction Defect Action Reform in Colorado

Construction Law

By Jennifer Seidman and Melissa L. “Mel” Roeder

Notes

citation Scarpati, “Overcoming Financial Procrastination for Legal Professionals,” 54 Colo. Law. 18 (Jan./Feb. 2025), https://cl.cobar.org/departments/breaking-the-cycle.

1. Pega et al., “Global, Regional, and National Burdens of Ischemic Heart Disease and Stroke Attributable to Exposure to Long Working Hours for 194 Countries, 2000–2016: A Systematic Analysis From the WHO/ILO Joint Estimates of the Work-Related Burden of Disease and Injury,” 154 Env’t Int’l (Sept. 2021), https://www.sciencedirect.com/science/article/pii/S0160412021002208.

2. Caruso, U.S. Advisor Metrics 2022: Trends in Advisor Compensation, Cerulli Associates, https://www.cerulli.com/reports/us-advisor-metrics-2022.

3. Napoletano, “Certified Financial Planner: What Is a CFP?,” Forbes Advisor (updated July 15, 2022), https://www.forbes.com/advisor/financial-advisor/what-is-a-cfp.