Affordable Housing Tax Exemptions in Colorado

December 2025

Download This Article (.pdf)

Willoughby Corner

(Lafayette, Colorado) is Boulder

County Housing Authority’s multiphase

affordable housing project. The project

has benefited from state and local tax

exemptions due to Boulder County

Housing Authority’s ownership interest

and will include about 400 housing units

at full build-out. (Photo courtesy of Molly

Chiang.)

This article explains property and sales and use tax exemptions for affordable housing projects in Colorado.

To incentivize the development and preservation of affordable housing in Colorado, the General Assembly enacted several tax exemptions for affordable housing projects. This article discusses property and sales and use tax exemptions under Colorado law and provides practice pointers for attorneys. This article is not intended to provide an exhaustive treatise on this topic. Rather, it aims to provide attorneys who advise affordable housing developers, lenders, investors, housing authorities, and local governments with an overview of the substantive law and a sense of how these exemptions work in practice.

The first section focuses on tax exemptions available through partnerships with local housing authorities. Research indicates that Colorado is one of only two states that empowers local housing authorities to grant these tax exemptions.1 The second section delves into the exemptions available to projects owned by nonprofits and community land trusts. The list of these exemptions grew with the passage of HB 23-1184 in 2023.

Affordable housing law is a hodgepodge of state and federal law. This article analyzes state tax law, but federal tax law—namely the federal Low-Income Housing Tax Credit (LIHTC) program—drives the financial structure of most affordable housing rental projects, and the US Department of Housing and Urban Development (HUD) plays a substantial role in regulating some of these projects.

Housing Authority Partnerships

The most utilized tax exemptions for affordable housing projects are rooted in Colorado’s Housing Authorities Law.2 The housing authority‑based exemptions are almost always used in affordable rental projects (as opposed to homeownership projects). Housing authorities can provide projects with exemptions (1) from sales and use taxes during construction and (2) from property taxes and special assessments for as long as the housing authority holds an ownership interest in the project.

The property tax exemption is especially valuable for affordable housing projects, which do not generate significant net operating income because of the restricted rents their residents pay. By eliminating a major operating expense, developers can build a viable project.

This section discusses which housing authorities can provide tax exemptions, what types of projects qualify, qualifying ownership structures, and other transactional considerations.

Types of Housing Authorities and Jurisdictional Boundaries

Three types of local housing authorities exist in Colorado—city, county, and multijurisdictional—all of which can confer the same tax exemptions. The Division of Local Government in the Colorado Department of Local Affairs maintains a list of housing authorities that have complied with the statutory filing requirements.3

A city housing authority shares geographical boundaries with the city that created it.4 For example, the Aurora Housing Authority’s boundaries are coterminous with the City of Aurora’s municipal boundaries.

A county housing authority shares boundaries with the county that created it, but its boundaries exclude any cities within the county unless a city passes a resolution authorizing the city’s inclusion within the county housing authority’s boundaries.5 For example, the Boulder County Housing Authority’s boundaries include all of unincorporated Boulder County and the City of Lafayette, which has authorized BCHA to operate within Lafayette’s boundaries.

A consortium of cities and counties can create a multijurisdictional housing authority, and its boundaries may include all (or less than all) of the cities, towns, and counties that created it.6 For example, the Chaffee Housing Authority is a multijurisdictional housing authority that operates in unincorporated Chaffee County, the City of Salida, and the Town of Buena Vista.

The Housing Authorities Law does not explain the significance of these boundaries and does not expressly limit a housing authority’s power to grant tax exemptions to its jurisdictional boundaries. For example, could the Denver Housing Authority hold an ownership interest in a housing project in Grand Junction? The Housing Authorities Law does not clearly answer this question.

Practitioners agree that the concept of boundaries would be meaningless if a housing authority’s powers were not confined to its jurisdictional boundaries. If a housing authority desires to develop or partner with a private developer for a project outside the housing authority’s geographical boundaries, the housing authority or developer should either seek a resolution from the local government with jurisdiction over the project that authorizes the housing authority to operate within the local government’s boundaries or enter into an intergovernmental agreement with the local housing authority.7

Partnerships

The Housing Authorities Law empowers housing authorities to “prepare, carry out, and operate projects” and “establish entities controlled by the [housing] authority that may . . . invest in as a partner or other participant or take any and all steps necessary or convenient to undertake or otherwise develop a project[.]”8 These provisions empower housing authorities to develop their own projects and partner with private nonprofit and for-profit developers.

“Projects”

The statute defines “project” broadly to include “buildings and improvements, . . . commercial facilities, and community facilities . . . to provide dwelling accommodations on financial terms within the means of persons of low income.”9 The inclusion of nonresidential improvements allows housing authorities to develop and partner in mixed‑use projects that include community-serving nonresidential uses like health care clinics, grocery stores, libraries, and childcare facilities. Housing authorities can also develop and partner in projects that include market-rate housing units “as long as the project substantially benefits persons of low income.”10

“Low Income”

The Housing Authorities Law has three key provisions that reference “persons of low income”:

- Projects that a housing authority may sponsor or partner in must “substantially benefit persons of low income.”11

- Only the portion of a project that “is occupied by persons of low income” qualifies for an exemption from property taxes and special assessments.12

- Sales and use tax and property tax exemptions are only available “in proportion to the percentage of the project that is for occupancy by persons of low income.”13

But the Housing Authorities Law does not define “low income.” Instead, it allows each housing authority to determine what constitutes low income based on local circumstances.14 Colorado housing authorities have not adopted a uniform standard. Most Front Range housing authorities follow HUD’s definition of “low income” as households earning at or below 80% of area median income.15 But housing authorities in the Western Slope and rural resort communities have granted tax exemptions to projects serving households earning at or below 140% of area median income.16 And, at the other end of the spectrum, at least one Front Range housing authority will only partner in projects that serve what HUD calls “extremely low‑income” households, which are households earning at or below 30% of area median income.

Determining what constitutes “low income” often becomes a key point of discussion and negotiation between the developer and housing authority, especially with rural housing authorities that may not have established partnership policies.17 On the one hand, most jurisdictions in Colorado are experiencing a shortage of affordable housing, and many affordable housing projects need the tax exemptions to be economically viable. On the other hand, these tax exemptions deprive governments of necessary tax revenue.

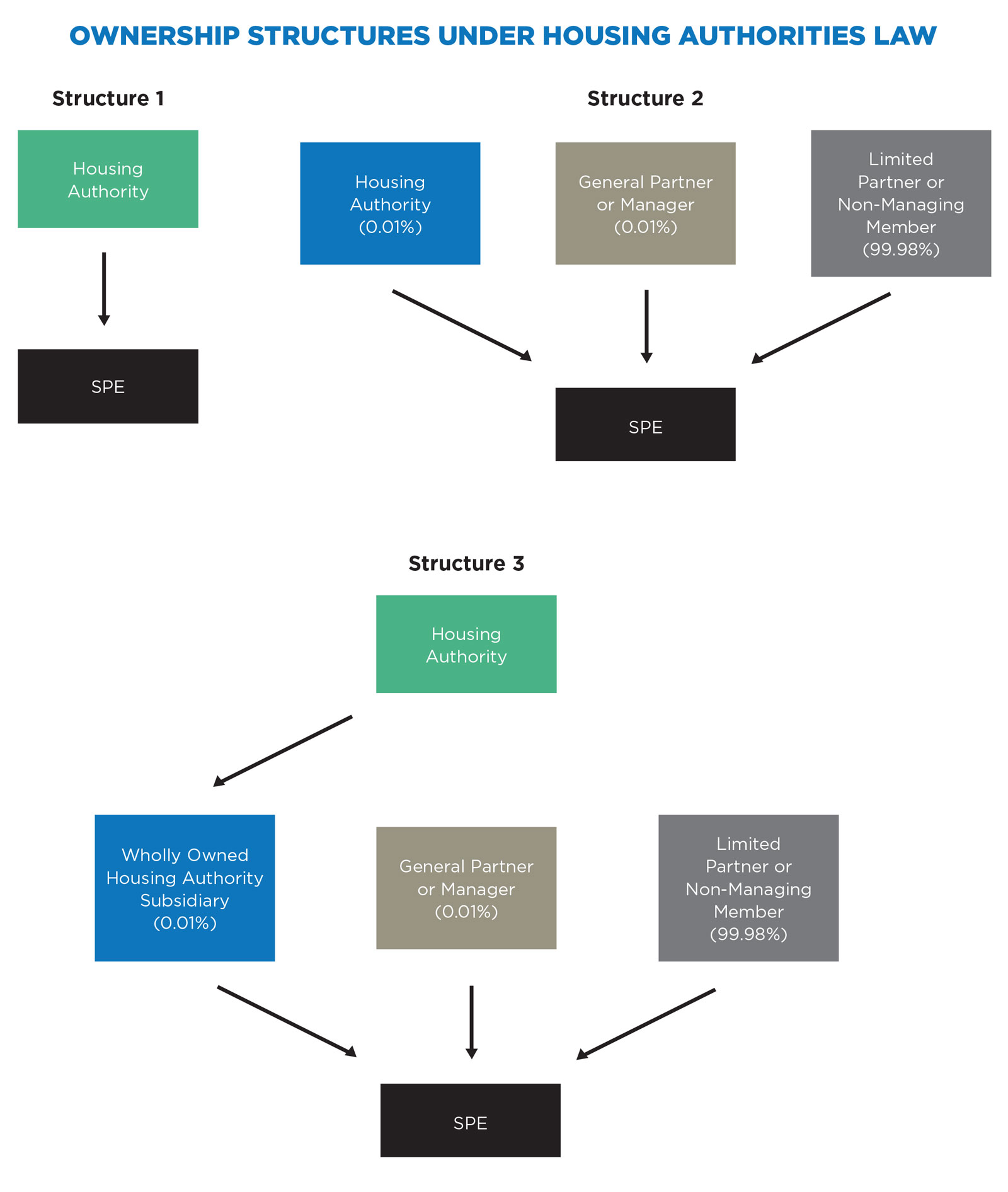

Ownership Structure

The tax exemptions under the Housing Authorities Law allow for three different ownership structures. All three structures require at least an element of ownership by the housing authority.18 In practice, most affordable rental housing projects (and most commercial real estate projects) are owned by single-purpose entities (SPEs), usually a limited liability company or limited partnership.19

The first structure is where the SPE that owns the project is wholly owned by a housing authority. This structure is rarely used.

The second structure is where the housing authority holds “an ownership interest” in the SPE that owns the project. This structure is the most common for newer projects developed by a housing authority (where the housing authority serves as the SPE’s general partner or manager) and projects developed by private developers where the housing authority serves as a special limited partner or non-managing member.

The third structure is where a wholly owned subsidiary of the housing authority holds “an ownership interest” in the SPE that owns the project. Some housing authorities in the Front Range use a nonprofit subsidiary to hold the housing authority’s ownership interests in projects developed by others.

The economics of the second and third structure drive down the housing authority’s ownership interest to a de minimis amount, usually 0.01%.20 For projects involving tax credits, the investor wants to capture as many of the tax benefits as possible, and these tax benefits are tied to their ownership percentage. Even in a more familiar joint venture structure used for non-tax credit orkforce or “missing middle” rental projects, the joint ventures usually divide up cash flow and capital proceeds according to ownership interest. In either scenario, there is not a compelling reason for the housing authority to hold more than a de minimis ownership interest.

In all three structures, the housing authority exerts very little control over the SPE. The SPE generally must comply with all affordability covenants, deliver periodic financial and operational reports to the housing authority, and pay the agreed-upon fees.

Tax Exemptions

The Housing Authorities Law provides qualifying projects with exemptions from property taxes and special assessments and from sales and use taxes during construction.

Property taxes. The Housing Authorities Law grants qualifying entities an exemption from all property taxes,21 including those levied by school districts, cities, counties, and other taxing districts.

This exemption is not processed through the Division of Property Taxation like other property tax exemptions. Instead, the housing authority or developer that partners with a housing authority submits a formal letter or property tax exemption certificate to the county assessor. The letter or certificate must state the housing authority’s percentage interest in the qualifying entity (or the percentage interest held by housing authority’s wholly owned subsidiary), the specific provision from the Housing Authorities Law that confers the exemption, and a statement about the portion of the project that qualifies for the exemption.

Most county assessors in the Front Range are familiar with the housing authority property tax exemption and implement it without further discussion. Many county assessors in rural areas are not familiar with the exemption, in which case the housing authority and developer may need to discuss the exemption with the county assessor and county attorney. Specifically, the housing authority and developer may need to explain how the ownership is structured and provide examples from other jurisdictions. The property tax exemption does not require subsequent compliance filings and should remain in effect until the housing authority no longer holds an ownership interest in the project.

Special assessments. The Housing Authorities Law also grants a qualifying project an exemption from “any special assessment to the state, any county, city and county, municipality, or other political subdivision of the state.”22 For newer neighborhoods on previously undeveloped land and major urban redevelopment projects, these special assessments can exceed the assessment for local property taxes.

Even though the definition of “project” in the Housing Authorities Law includes nonresidential improvements, the exemption from special assessments does not extend to commercial facilities or market-rate housing.23

This exemption presents challenges when the land lies within a special district—such as a fire, water, or sanitation district—or a general improvement or metropolitan district formed to finance infrastructure within a larger planned area. In practice, metropolitan districts have generally excluded affordable housing projects from the district rather than allowing the project to avail itself of the exemption. Some districts negotiate for a lump-sum payment in lieu of annual assessments. Special districts are experimenting with ways to circumvent this exemption. For example, some metropolitan districts are recording stand-alone covenants in which the owner and its successors in title agree to pay special assessments notwithstanding any exemption.

Sales and use tax. The Housing Authorities Law grants qualifying entities an exemption from sales and use taxes “to the state or any county, city and county, municipality, or other political subdivision of the state” during construction.24 In practice, this exemption applies to all materials purchased for the project through completion and the issuance of a certificate of occupancy. The exemption also applies to fixtures and appliances.25 Like the exemption from special assessments, the sales and use tax exemption does not extend to commercial facilities or market-rate housing.26

Construction costs are the single largest expense for most housing projects, and building materials usually make up around half of construction costs. This exemption reduces the cost of building materials by between 5% and 10%, depending on the jurisdiction’s combined tax rate.

To obtain a tax exemption certificate from the Colorado Department of Revenue, the qualifying entity must submit Form DR 0715 and a sales and use tax exemption certificate from the housing authority with project details.27 Once approved, the entity’s general contractor must submit Form DR 0172 to receive the exemption certificate, which can then be shared with subcontractors and material suppliers.

Partial Exemption

All three tax exemptions are limited to the portion of the project “that is for occupancy” or “is occupied” by low-income households.28

For mixed-use and mixed-income projects, the Housing Authorities Law allows the housing authority to grant a partial exemption based on relative square footage or cost of a project that serves low‑income households.29 For example, consider a mixed-use project with a café on the ground floor and low‑income housing units on the four floors above the café. If the café occupies 20% of the building, but the cost of its construction makes up only 15% of the total project costs, then the housing authority could grant sales, use, and property tax exemptions for 80% or 85% of the project depending on whether it takes the square footage or cost approach.

The partial exemption provisions also allow housing authorities to partner in mixed-income projects. For example, consider a 100-unit project with 50 units of market-rate housing and 50 units of affordable housing. If the market-rate units occupy 50% of the building, but the cost of their construction makes up 55% of the total project costs, then the housing authority could grant sales, use, and property tax exemptions for 50% or 45% of the project.

the Northeast Denver Housing Center.)

Ground Leases

The Housing Authorities Law’s tax exemptions extend to “[a] project . . . leased to” a qualifying entity.30 Affordable housing projects often use ground lease structures for public policy and tax reasons. At least a few county assessors in the Front Range have determined that if the ground lease requires the affordable housing project (the ground lessee) to pay property taxes, then the property tax exemption extends to both the leasehold interest and the landlord’s fee interest.

Housing Authority Fees and Purchase Rights

Housing authorities usually charge fees to partner in affordable housing projects sponsored by private developers and frequently negotiate rights to eventually purchase the project. These fees and purchase rights vary from jurisdiction to jurisdiction and from project to project. Larger housing authorities with established partnership programs tend to charge higher fees and impose ongoing compliance obligations, while smaller housing authorities tend to play a limited role in project oversight and charge lower fees.

At a minimum, housing authorities usually require their development partners to reimburse them for out‑of-pocket legal and due diligence expenses. For projects serving extremely low‑income households and projects sponsored by nonprofit developers, housing authorities typically reduce their fees or do not charge beyond the initial reimbursement at closing. Some housing authorities require projects to pay an annual asset management fee or a one-time payment in lieu of taxes, which housing authorities calculate based on the value of tax savings conferred by the housing authority’s participation. The asset management fee is typically fixed and increases annually by a set percentage. Some projects pay the payment in lieu of taxes annually, and others pay it upfront at the closing of their construction financing. Housing authorities and developers can structure these fees in different ways to best suit the project’s financial needs.

Home Rule Question

Some home rule jurisdictions, including Denver and Colorado Springs, have taken the position that the local component of sales and use taxes is a matter of purely local concern, in which case (these jurisdictions argue) the home rule jurisdiction’s sales and use tax regime would prevail over the tax exemption in the Housing Authorities Law.31 Although this issue has not been litigated under the Housing Authorities Law, precedent favors this position.32 In a recent case, a Denver district court held that home rule jurisdictions’ sales and use taxes prevailed over a state statute that purported to grant a sales and use tax exemption for public school construction and maintenance.33

Developers working in home rule jurisdictions should proactively engage with the local government to determine whether the jurisdiction will honor the exemption. If it will honor the exemption, the developer should seek a resolution from its governing body. If it will not honor the exemption, the developer will need to engage with their general contractor to accurately include local sales and use taxes in their construction budget.

Recent Trends

Until recently, the tax exemptions available under the Housing Authorities Law were most frequently used in projects financed with federal LIHTC. These projects usually restrict occupancy to households earning at or below 60% of area median income.34

Recent legislative changes at the federal and state level have expanded the use of housing authority tax exemptions to benefit projects with higher-income households.

First, a legislative change in 2018 to the federal LIHTC program allows LIHTC projects to serve households earning up to 80% of area median income as long as the project’s average household income equals 60% or less of area median income.35 In practice, housing authorities have been willing to determine that the entire project—even the units that serve households earning up to 80% of area median income—benefit persons of low income.

Second, pandemic-era federal funding (mostly from the State and Local Fiscal Recovery Funds component of the American Rescue Plan Act) and Proposition 12336 have funneled resources to so‑called workforce or “missing middle” housing projects—projects serving households earning between 80% and 120% of area median income. The new funding sources have increased interest in this market segment among affordable and market-rate developers. Housing authorities are frequently granting full or partial tax exemptions to these projects.

Another noteworthy legislative change involves the creation of a statewide Middle Income Housing Authority in 2022.37 Although discussion of the Middle Income Housing Authority’s full powers is beyond the scope of this article, the Middle-Income Housing Authority Act exempts “the affordable housing component” of its properties from property and sales and use taxes.38

Nonprofit Tax Exemptions for Affordable Housing

In addition to the tax exemptions available under the Housing Authorities Law, Colorado provides affordable housing projects sponsored by nonprofit developers with other avenues for exemptions. The General Assembly expanded the types of affordable housing projects that qualify for exemptions under HB 23-1184.39 The second half of this article discusses five separate exemptions. Exemptions available for transitional housing, assisted living facilities, and orphanages are beyond the scope of this article.

All five exemptions discussed below are codified in Title 39. The first three exemptions are only available to affordable housing rental projects sponsored by nonprofit developers.40 The next two exemptions are only available to nonprofits and community land trusts developing for-sale affordable housing.41

These exemptions are not self-executing. For each exemption, the property owner must complete a general exemption application and exemption-specific supplements from the Division of Property Taxation (division) within the Colorado Department of Local Affairs. The staff of the exemptions section within the division is knowledgeable and can help with choosing the correct forms. Practitioners and developers should anticipate a six- to twelve-month review and approval timeline, onsite inspections, and follow-up questions from the division.

Property Tax Exemptions for Nonprofit Rental Housing

Title 39 includes property tax exemptions for three types of affordable rental projects sponsored by nonprofit developers.42

These exemptions begin once construction commences if the “property is irrevocably committed to residential use” in accordance with the exemption’s requirements.43 Although the statute does not define “irrevocably committed to residential use,” under current administrative practice, a long-term use and occupancy covenant provides sufficient evidence of the applicant’s commitment to the exemption’s affordability requirements.

For each project type, the property owner must demonstrate that the project is “efficiently operated.”44 The division assesses efficiency by examining the reasonableness of the project’s operating costs, among other factors.45

Like the exemptions available under the Housing Authorities Law, the division may grant a partial exemption if less than the entire project is occupied by qualified households.46 If the division grants the initial exemption, the property owner must submit an annual occupancy report to the division.47 If the property owner does not already obtain resident income certifications for HUD, the Colorado Housing and Finance Authority, or the Colorado Division of Housing, then the property owner must obtain stand-alone certifications for the division.

Elderly or disabled low-income residential facility. The first exemption is available for nonprofit‑sponsored affordable housing projects that serve low-income senior or disabled households.48 Senior (age 62 or older) or disabled individuals or any household with a senior or disabled head of house or spouse meet the exemption’s requirement.49

To qualify for the exemption, the property owner must also limit occupancy to households earning at or below 150% of the “limits prescribed for similar individuals or families who occupy low-rent public housing operated by a city or county housing authority which is nearest in distance” to the project.50 In practice, the division interprets “limits prescribed for . . . low-rent public housing” to mean households earning at or below 80% of area median income.

Low-income households. The second exemption is available for nonprofit‑sponsored affordable housing rental projects that serve households earning less than 30% of area median income.51 The property owner seeking this exemption must also demonstrate that the project’s rents are lower than a comparable housing unit for which the exemption does not apply by “at least the value” of the exemption.52 The division uses Fair Market Rent calculated by HUD as a proxy for “comparable housing unit[s].” In practice, projects that serve these extremely low-income households are only economically viable with Project-Based Section 8 vouchers.

Single-parent families in a family service facility. The third exemption is available for nonprofit‑sponsored affordable housing rental projects that serve “single‑parent families.”53 The statute does not define single‑parent families.

Like the property tax exemption for elderly and disabled housing, the property owner must demonstrate that the households’ incomes are at or below 150% of the “limits prescribed for similar individuals or families who occupy low-rent public housing operated by [the local housing authority].”54 In addition to the restrictions on family composition and income, the project seeking the exemption must also provide its residents with counseling services and an on-site licensed childcare facility.55

Property Tax Exemptions for For-Sale Affordable Housing

In 2023, the General Assembly passed and the governor signed HB 23-1184, which granted property tax exemptions to nonprofits and community land trusts that develop for‑sale affordable housing.56 The first exemption grants nonprofit developers and community land trusts a property tax exemption while they hold vacant land and construct the project.57 The second exempts land owned by a nonprofit or community land trust held under a long-term ground lease.58

Pre-sale exemption. Beginning in property tax year 2024, property on which a nonprofit housing developer intends to construct or rehabilitate housing to eventually sell to income-qualifying households is exempt from property taxes.59

Qualifying households cannot earn more than 100% of area median income except in rural resort communities, where they can earn up to 120%.60 The statute provides examples of “indicators” of a nonprofit’s intent to develop for-sale affordable housing.61

The exemption’s availability begins when the nonprofit housing developer acquires the property and ends when it either conveys the property without developing affordable housing or sells the housing units to income-qualified buyers.62 If the nonprofit conveys the property without selling affordable housing to a qualified household or other nonprofit housing developer, it must repay all property taxes that would have been collected but for the exemption.63 If the nonprofit develops the property and sells units to income-qualified buyers, the exemption ends when the local government issues a certificate of occupancy for the unit.64

Community land trust property. HB 23-1184 also included a stand-alone exemption for community land trust property.65 In a community land trust, the trust retains fee title to the underlying property and leases the underlying property and sells the improvements to an income‑qualified homebuyer. This transaction results in two separate taxable parcels: one for the community land trust’s fee interest in the underlying property, and another for the homeowner’s interest in the improvements.

HB 23-1184 granted a property tax exemption for the community land trust’s fee interest in the underlying dirt and clarifies that the exemption does not extend to the homeowner’s improvements.66 Like the exemption for land owned by a nonprofit affordable housing developer on which it intends to construct affordable housing, if the trust later conveys the property such that it no longer qualifies as an affordable homeownership property, the trust must repay all property taxes that would have been collected but for the exemption.67

To claim the exemption, the community land trust must submit the land lease to the county assessor to create the separate tax parcels. The trust must also complete and submit a general exemption application and an exemption-specific supplemental form to the Division of Property Taxation, and if the exemption is granted, file annual exemption reports.68

Conclusion

Colorado law incentivizes the development of affordable housing through tax exemptions. For most affordable rental projects, developers partner with the local housing authority. These partnerships unlock sales, use, and property tax exemptions that make these projects economically viable. Colorado law provides other property tax exemptions for affordable rental projects owned by nonprofits and for for-sale affordable housing projects developed by nonprofits and community land trusts.

Explore This Issue

Standing Out Thoughtfully

Mentor in Law

By Nyssa P. Chopra

Related Topics

Notes

citation Gano, “Affordable Housing Tax Exemptions in Colorado,” 54 Colo. Law. 32 (Dec. 2025), https://cl.cobar.org/features/affordable-housing-tax-exemptions-in-colorado.

1. Texas allows local government units (including housing authorities) to create subsidiaries called Public Facility Corporations that exempt affordable housing projects from ad valorem taxes.

2. CRS §§ 29-4-201 to -230.

3. Colorado Department of Local Affairs, Division of Local Government, Local Government Information System, https://dola.colorado.gov/dlg_lgis_ui_pu/.

4. CRS § 29-4-204(5).

5. CRS § 29-5-508.

6. CRS § 29-1-204.5.

7. See CRS § 29-20-105 (authorizing and encouraging the use of intergovernmental agreements “for the purposes of planning or regulating the development of land”).

8. CRS § 29-4-209(1)(d), (d.7).

9. CRS §§ 29-4-203(12), -226(1)(d), -227(1)(b).

10. CRS § 29-4-203(12).

11. Id. (emphasis added).

12. CRS § 29-4-226(1)(d) (emphasis added).

13. CRS § 29-4-227(1)(b) (emphasis added).

14. See CRS §§ 29-4-203(12) (granting housing authorities the discretion to determine whether a project “substantially benefits persons of low income”), -227(1)(b) (a housing authority’s determination of the percentage of the project that is for occupancy by persons of low income “is presumed valid absent manifest error”).

15. See, e.g., Denver Housing Authority, Special Limited Partnership Development Participation Policy (Nov. 21, 2024), https://www.denverhousing.org/affordable-housing-developers; Housing Authority of the City of Aurora, Partnership Criteria Policy (Aug. 11, 2022), https://irp.cdn-website.com/cb9d28f1/files/uploaded/SLP%20Policy%20Amended%20Aug%202022_zt2xqGj2QKKXfP6Xe5FM.pdf; Maiker Housing Partners, Special Limited Partnership Development Participation Policy (Mar. 19, 2020), https://maikerhp.org/wp-content/uploads/2020/11/Maiker-Development-Participation-Policy-200319.pdf.

16. See, e.g., Chaffee Housing Authority, Resolution No. 2023-18, 2023, https://www.chaffeehousingauthority.org/realestateprojects/carbonatestreet (granting tax exemptions for workforce housing project in Buena Vista serving households earning 80% to 120% of area median income).

17. Front Range housing authorities participate in projects more frequently than rural housing authorities. To prevent renegotiating terms on every project, and to treat similarly situated developers similarly, Front Range housing authorities tend to adhere to written partnership policies that are updated periodically.

18. CRS §§ 29-4-226(1), -227(1)(b).

19. Because most affordable rental housing projects are financed in part with tax credits—almost always federal LIHTC—developers structure these entities as LLC or limited partnerships where the developer owns a nominal interest (0.01%) and the tax credit investor owns almost all of the membership or partnership interests (99.99%).

20. Practitioners have not settled on how small an ownership interest can be to be treated as an ownership interest under state law and federal tax law. It is not uncommon to see partnership or membership interests as low as 0.005% in these structures.

21. CRS § 29-4-227(1)(b).

22. CRS § 29-4-226(1).

23. CRS § 29-4-226(1)(d).

24. CRS § 29-4-227(1)(b). See also CRS § 39-26-704(1.5) (authorizing the sales and use tax exemption).

25. Colorado Department of Revenue, Taxpayer Service Division, Sales 95: Sales/Use Tax Exemption for Affordable Housing Projects (2016), https://tax.colorado.gov/sites/tax/files/Sales%2095.pdf.

26. CRS § 29-4-227(1)(b).

27. Colorado Department of Revenue, supra note 25.

28. CRS §§ 29-4-226(1)(d) (limiting the exemption from special assessments), -227(1)(b) (limiting the exemption from sales and use and property taxes).

29. CRS § 29-4-227(1)(b).

30. Id.

31. See Colo. Const. art. XX, § 6; City & Cnty. of Denv. v. State, 788 P.2d 764 (Colo. 1990).

32. Winslow Constr. Co. v. City & Cnty. of Denv., 960 P.2d 685 (Colo. 1998).

33. City & Cnty. of Denv. v. State, Case No. 2022CV31841 (Denv.Dist.Ct. Nov. 23, 2022).

34. IRC § 42(g)(1)(C).

35. 26 CFR § 1.42-19.

36. CRS §§ 29-32-101 et seq.

37. SB 22-232.

38. CRS § 29-4-1104(12)(a).

39. CRS §§ 39-2-113.5, 39-2-117, 39-3-127.7.

40. CRS § 39-3-112(3)(c).

41. CRS §§ 39-3-113.5, -127.7.

42. CRS §§ 39-3-113.5, -127.7.

43. CRS § 39-3-113.

44. CRS § 39-3-112(3)(b).

45. CRS § 39-3-112(3)(b)(I).

46. CRS § 39-3-112(4).

47. CRS § 39-2-117(3)(a)(I).

48. CRS § 39-3-112(1)(a.3), (a.5), (2), (3)(a)(II)(A).

49. Id.

50. Id.

51. CRS § 39-3-112(1)(b.3), (2), (3)(a)(II)(C).

52. CRS § 39-3-112(1)(b.5)(III).

53. CRS § 39-3-112(2), (3)(a)(II)(B).

54. CRS § 39-3-112(3)(a)(II)(A).

55. CRS § 39-3-112(1)(b).

56. CRS §§ 39-2-113.5, 39-2-117, 39-3-127.7.

57. CRS § 39-3-113.5.

58. CRS § 39-3-127.7.

59. CRS § 39-3-113.5(2)(b)(I).

60. CRS § 39-3-113.5(1)(c)(II).

61. CRS § 39-3-113.5(2)(c)(II).

62. CRS § 39-3-113.5(2)(b)(I).

63. CRS § 39-3-113.5(3)(b)(III).

64. CRS § 39-3-113.5(2)(b)(II).

65. CRS § 39-3-127.7.

66. CRS § 39-3-127.7(3), (5).

67. CRS § 39-3-127.7(4).

68. CRS § 39-3-127.7(6), (7).